Investing in a home during inflation: timing is everything

With inflation running historically high, is it a good time to purchase a home?

Hi everyone,

As you may already know, I started this newsletter to share my learnings after a decade of working at world-class vertically integrated real estate companies, private equity firms and startups. We will be discussing and advising on a wide range of topics, spanning from a technical investment analysis of public Real Estate Investment Trusts to preparing for and nailing a real estate interview. Top of my mind is America’s excruciating housing affordability crisis. Therefore, much of the content will focus around shedding light on this huge challenge facing our society today and working toward a solution as a community. A key part of this is how and when to buy a home to make it an investment. So this week, for our first publication, we’re going to start with a basic exercise that affects (hopefully) all of us at some point in our lives: what’s a good time to buy a home? Next week - we’ll turn to how a private real estate investment in a home or small rental property compares to investing in publicly listed real estate stocks. Let’s jump in.

Investing in a home during inflation: timing is everything

Nobody has a crystal ball. So whether it’s a newsletter author, your mom or dad, your financial manager, or Warren Buffet, it’s a safe bet that nobody can provide a perfect answer to the age old question: is it the right time to buy a house? The amazing thing about home buying is, with the right knowledge, any of those people just mentioned could give a pretty good guesstimate (at least financially) - down to the year, and even the month. Housing markets, unlike stocks, crypto, and many other asset classes, move fairly predictably over time due to a handful of factors. Not everyone has the luxury of timing their purchase perfectly. Sometimes as buyers, we just moved to a new city, had a second child, or needed to downsize. That said, for nearly everybody, a house is the biggest financial decision we will ever make. So let’s do some quick homework together now to answer the question: with inflation high and rates moving to historically elevated levels, is now a good time to buy a home?

What dictates the price of housing?

We’re able to get to an answer pretty quickly on this one because when it comes to single family homes, the price of housing moves due to a handful of inputs. I could give you the laundry list: job drivers, population growth, geography, microlocation, supply and demand, etc. However, there is just one key input:

Money supply

Take a look at the graph below:

What you’re looking at above is the historic rise of housing prices over the last three years which coincided with loose Fed policy (i.e. quantitative easing) during the pandemic. With a slight lag, the average price of homes across the US changes almost exactly proportionally with the US Money Supply. Now, understanding that “money supply” doesn’t mean much to most readers besides maybe a few economics and finance majors, let’s simplify further.

Most determinant factor of money supply = Fed Policy

Primary Fed policy mechanism = Rates

So what affects the price of homes? Rates. Rates are the most important factor in single-family home prices, and the cool thing about rates is that they are set and communicated by the Fed, both absolutely and directionally. In other words, as consumers, we always know how much they are and generally also know whether they’re going up or down in the near future. How? The Federal Reserve of the United States tells us.

So, which rates? How much are they? And where are they headed?

When we say rates, as it relates to housing, it usually refers to one of the following:

Fed Funds Rate: currently 3.83%

Mortgage Rates: currently 6.33% (30-year, fixed)

First, the Fed sets their “target interest rate” or Fed funds rate. Then, mortgage providers set the price of their loans i.e. “mortgage rates” based on the Fed funds rate. This is sort of a two-step process which happens so fast that for home-buying purposes we can think of it as simultaneous. Over the last handful of months, due to interest rate hikes at the Fed, mortgage rates have risen to levels not seen in years.

Mortgage rates, in turn, drive the “cost of housing.” Consider this: a year ago, your mortgage payment on a $500,000 house would have been $2,028, at today’s rates that same payment is $3,226 (a 59% increase). Additionally, the cost of housing has become significantly more burdensome as a percentage of overall income:

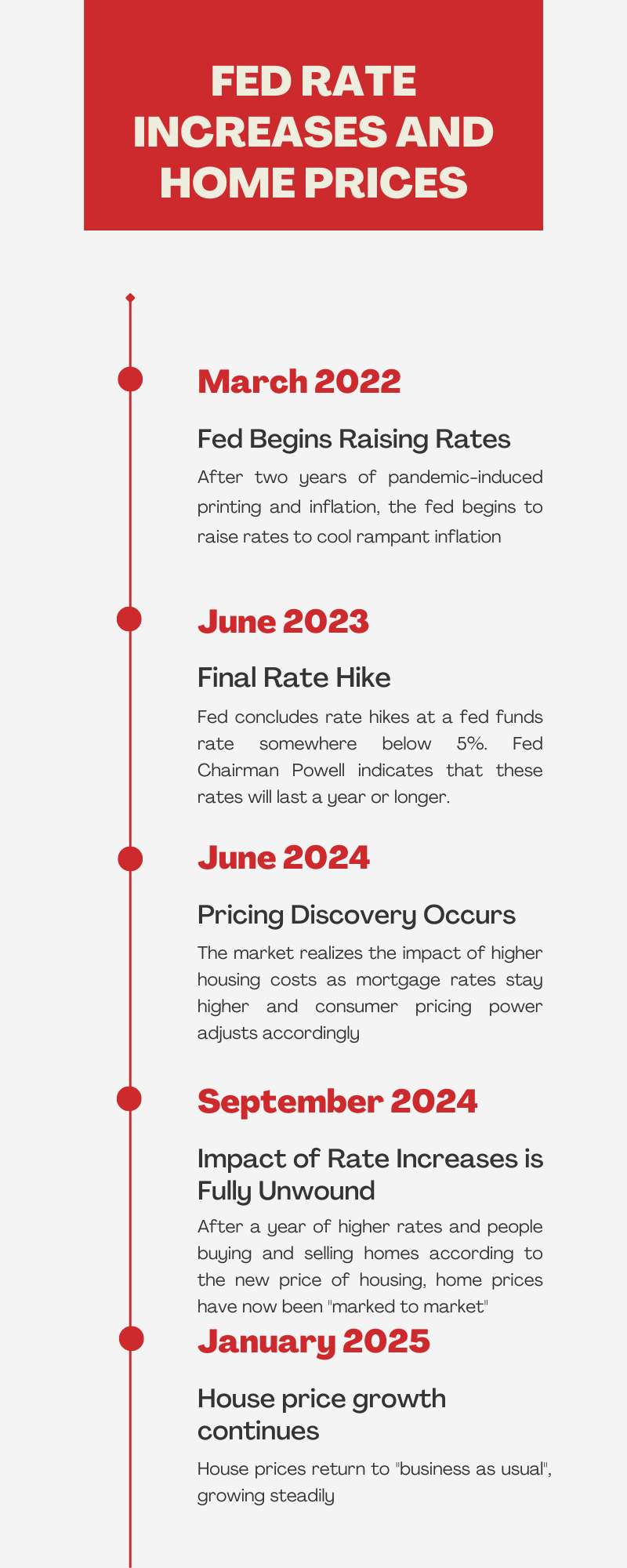

What does the Fed tell us about rates over the immediate future?

There are going to be at least two more “hikes”, or increases, over the next few months. In total, these raises will be about 0.75%-1.00%. One of them is today on 12/14/22 for a 0.50% increase

Rates will then stay at that higher ultimate rate (~5% Fed funds rate) for longer, perhaps longer than 12 months, until inflation is in check

Will this affect the price of housing? Absolutely.

18-24 months from now is the sweet spot for a purchase

If it’s really this easy to predict the cost of housing, then why doesn’t everybody buy at the right time, and do well on their home investment?

The answer lies in a simple concept that investors in the real estate industry love: mark to market. Understanding mark to market is what gives savvy real estate investors the ability to beat returns in almost any other investment class including mutual funds, stock market indexes like the Dow and S&P, or even many VCs and hedge funds. Mark to market put simply: real estate takes time, because it’s expensive, and takes longer to trade.

The best way to understand this is through an example. Let’s think about a popular stock like Apple, as compared to the price of a home we might consider buying, and let’s think about how the price of each changes with respect to rates:

Apple: traders on wall street have know that rates are going to go higher weeks and months ahead of the Fed announcing it, and since they move most of the money that’s invested in a company like Apple, the price of the stock is reflected accordingly. In fact, most professional traders and investors will tell you that the “fair price” of Apple was set by the market 6-9 months ago, and included the impact of rates. How?

Because millions of dollars worth of Apple trade hands every minute on public exchanges. With each exchange, someone is aware of a new piece of news or information, and many of those exchanges are driven by traders who are aiming to make a short term profit. Therefore, a new and efficient price of Apple is every second, based on a lot of data points, or instances. Another way to think about this is that the stock market looks 6-9 months into the future.

The House: people buy and sell houses for very different reasons. Its true that private equity and public investors have increasingly been focusing on single family homes. That said, a vast majority of homes are still bought and sold by regular Americans, most of whom do not follow the Fed’s actions every day and all of whom are working with limited pricing information. Why?

Houses “trade”, i.e. are bought or sold, rarely. A house can go 10 years with only one sale and it’s during that sale, when a buyer steps up and says “yes, I will pay this many dollars for that home” that we truly find out what it’s worth. This is the one concrete way to “mark to market”; which means valuing an asset according to current market conditions. Since trades are rare, most homes are valued according to comparable trades or “comps” that have sold over the previous 4-8 months. Therefore, whereas a house that was sold a year ago for $1,000,000 might be on the market for $900,000 today because homes in the same neighborhood traded in that range 4-8 months ago, today’s fair value may be lower based on what somebody would actually pay for the house

To summarize, there’s a lag in the price of homes. That’s why when the housing bubble burst in 2008 and so many owners were forced to sell their homes, it still took 2 full years before home prices finally bottomed in 2010, and another 2 years before they started moving upwards again in 2012. It takes time for “price discovery” to occur.

Now, let’s look at our recent timeline of events to determine whether it’s the right time to buy in this inflationary and rising rate environment.

Therefore, if history is any indication and rates have the effect we think they will, the time to buy a home will be in 18-24 months, roughly in the fall or winter of 2024.

I got the timing right! But, I’m still anxious, will my house be a good investment?

Now for the best part. Going back to 1960 (as far as good data is available), the average home price in the US has always been higher 5 years after any given point in time. With only a handful of brief and shallow drawdowns in price, chief among which was the Great Financial Crisis/mortgage bubble collapse of 2008. Historically, housing prices don’t really go down and, when they do, they tend to recover within a few short months or years. Given the investment horizon for most buyers, or how long they plan to own the home before selling, chances are they will end up selling the home for more than they purchased it. It still makes sound financial sense to time a purchase as best as we can to enjoy the benefits of rising prices during periods of increasing money supply, really what we’re doing here is optimizing upside. Downside, when it comes to a house purchase, is limited.